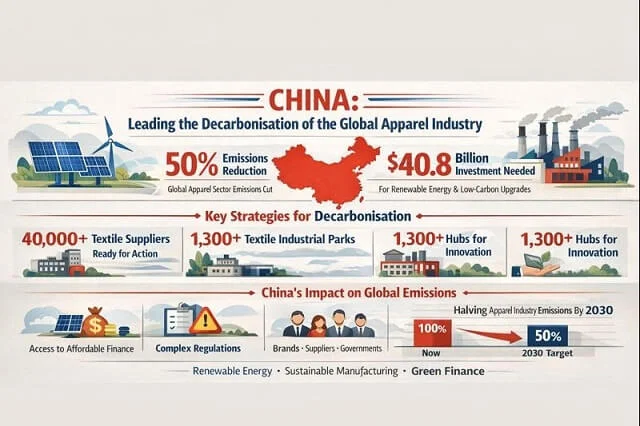

China’s Textile Sector could play a decisive role in cutting greenhouse gas emissions across the global apparel industry, with the potential to reduce sector-wide emissions by as much as 50% by 2030, according to a new report by the Apparel Impact Institute (AII) in collaboration with Development Finance International Inc. (DFI).

The report, Landscape and Opportunities for the Decarbonization of China’s Textile and Apparel Manufacturing Sector, outlines how China’s unmatched scale in textile and apparel production combined with its rapid progress in renewable energy deployment by creating a unique opportunity to accelerate climate action across one of the world’s most carbon-intensive industries.

China remains the world’s largest apparel and textile manufacturing hub, hosting more than 40,000 suppliers with established operational data, energy usage records and production scale. This depth of data and industrial maturity positions manufacturers to move quickly from pilot projects to large-scale emissions reductions.

The report also highlights China’s extensive industrial park ecosystem as a key structural advantage. More than 1,300 textile-focused industrial parks, housing over 11,000 enterprises, offer a ready-made platform for shared governance, pooled investment and coordinated decarbonization initiatives.

By aggregating demand for renewable energy, energy-efficient machinery and low-carbon infrastructure, these parks can significantly lower transition costs and implementation risks for individual suppliers.

Also Read : France Targets Ultra-Fast Fashion With New Eco Taxes

Despite China’s technical readiness, the report identifies access to affordable finance as the primary constraint to rapid decarbonization. Achieving a 50% emissions reduction by 2030 will require an estimated US$40.8 billion in investment across renewable energy, energy efficiency upgrades and low-carbon manufacturing technologies.

While international financial institutions and climate funds are increasingly active in sustainable manufacturing, supplier uptake has been limited.Complex compliance requirements, lengthy approval processes and higher borrowing costs have reduced participation, particularly among small and mid-sized manufacturers.

To bridge this gap, the report recommends scaling blended finance mechanisms, deployment-linked grants and locally administered technical assistance. Integrating low-carbon investment planning into core business strategies rather than treating sustainability as a parallel initiative is also seen as essential for long-term impact.

The study stresses that meaningful emissions reductions will require closer collaboration between brands, manufacturers, policymakers and financial institutions. Industrial parks are identified as ideal hubs for coordinated action, enabling shared infrastructure such as rooftop solar, centralized energy management systems and wastewater treatment facilities.

Also Read : Rebalancing The Yarn Equation In Bangladesh’s Apparel Industry

“China’s textile industry has the scale, capability and growing alignment to lead fashion’s next climate chapter,” said Dave de la Questa, Head of Asia Operations at Development Finance International.

Lewis Perkins, President and CEO of the Apparel Impact Institute said, “Scaling local finance, improving supplier readiness and investing in collaborative infrastructure will determine whether emissions reductions move from ambition to reality”.

If China successfully accelerates decarbonization across its textile and apparel sector, the impact would extend far beyond national borders. Given China’s central role in global sourcing, emissions reductions achieved there would significantly lower the carbon footprint of apparel brands worldwide.

As brands face tightening climate targets and regulatory scrutiny, China’s ability to align industrial policy, finance and manufacturing capacity could reshape the pace and structure of decarbonization across the global fashion industry.

{kind=link}