Argentina’s textile industry is facing one of its deepest downturns in nearly a decade, as a sharp rise in imported garments continues to erode domestic production, weaken factory utilization, and accelerate job losses, according to industry data and trade analysis.

Recent figures from the Argentine Textile Industries Federation (FITA) show the textile industrial production index plunged 23.9% year-on-year in January 2026, marking its lowest level since records began in 2016.

The contraction has been particularly severe in key segments such as fabrics, finishing, and cotton yarns, all of which recorded declines exceeding 30%, significantly underperforming the broader manufacturing sector, which slipped just 3.2% over the same period.

The downturn reflects a longer-term structural decline. Data from the Pro Tejer Foundation indicates that textile production has fallen 27.8% compared to two years ago, underscoring persistent weakness across the sector.

Perhaps most striking is the collapse in capacity utilization, which dropped to just 24% in January 2026, less than half the national industrial average of 53.6%. This signals widespread underuse of machinery and idle production lines across the country’s textile hubs.

At the same time, employment in the sector has deteriorated sharply. Industry groups report that textiles, apparel, leather, and footwear collectively lost 12,000 formal jobs over the past year, bringing total employment down to around 100,000 as of December 2025. Since late 2023, cumulative job losses have exceeded 20,000, making textiles the worst-performing sector in terms of employment decline within Argentina’s private economy.

The crisis has unfolded alongside rapid growth in digital commerce, which has fundamentally reshaped consumer behavior. Argentina’s e-commerce market expanded by 55% in 2025, significantly outpacing inflation, which stood at 31.5%.

However, this growth has increasingly favored international platforms, with 47% of online shoppers now purchasing goods from abroad. Cross-border platforms such as Temu and Shein dominate this segment, capturing 41% and 31% of overseas purchases respectively, while traditional global players lag behind.

Domestic brands and retailers are struggling to compete in this shifting landscape. Local e-commerce platform Tiendanube reported a 14% drop in nominal revenue for non-sports apparel, attributing much of the decline to competition from low-cost imported goods, particularly from China.

Small and medium-sized enterprises are especially vulnerable, with 88% citing falling sales as their primary challenge and over two-thirds identifying imports as a major threat.

Source: DataLiner

Also Read: Argentina’s Textile Industry Crashes Amid Import Surge

Trade data reinforces the scale of the shift. Imports of finished garments surged dramatically in early 2026, rising 54% in volume and 27% in value in February alone. Over the first two months of the year, apparel imports jumped 82% in tonnage and 53% in dollar terms, highlighting strong inbound demand for foreign-made clothing.

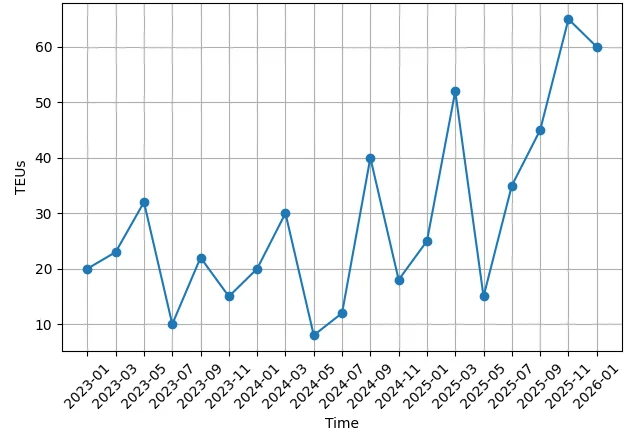

Containerized shipping data provides further insight into the trend. Imports of fabric garments, measured in TEUs (Twenty-foot Equivalent Units), have shown a clear upward trajectory since 2023, with a notable spike in early 2026.

The chart illustrates a steady increase in inbound garment shipments, culminating in a sharp rise in early 2026, when volumes reached their highest levels in the observed period. This aligns with reports of a 39% surge in TEU volumes during January and February, indicating a significant influx of imported goods into the domestic market.

In contrast, imports of critical production inputs such as yarns, raw materials, and fabrics have declined sharply, falling more than 35% in volume and over 50% in value. This divergence suggests that local manufacturers are scaling back operations due to weak demand and intensifying competition, while consumers increasingly rely on finished imported products.

Industry groups have also raised concerns about widespread under-invoicing practices. FITA estimates that more than 70% of textile imports are declared at values significantly below historical norms, with some goods reportedly priced below raw material costs.

Examples include cotton T-shirts imported for less than $0.01, jeans under $1, and towels priced below $0.30 per kilogram. Such pricing distortions are seen as creating unfair competition and further undermining domestic producers.

Import volumes have surged to record levels. In the first ten months of 2025, Argentina imported 332,696 tonnes of textiles and apparel, up 89% year-on-year. Within this, finished goods and garments saw increases of 217% and 166% respectively, reflecting a structural shift toward import dependence.

The pressure is also evident in market share dynamics. Around 37% of industrial SMEs reported losing domestic market share due to foreign competition—the highest level recorded since 2007. China remains the dominant source of imports, identified as the primary competitive threat by over 73% of firms.

Despite these challenges, consumer prices have not risen in line with industry strain. The clothing, leather, and footwear category recorded no monthly price increase in February 2026. However, industry analysts note that this stability masks deeper issues, including negative profit margins and widespread below-cost selling, as firms attempt to remain competitive in a market increasingly dominated by cheaper imports.

As Argentina’s textile sector grapples with declining output, rising imports, and structural shifts in consumer demand, industry stakeholders warn that without targeted policy interventions, the country risks further deindustrialization and long-term loss of manufacturing capacity.

{kind=link}