The year 2026 represents more than a calendar milestone for the global garment industry; it marks the beginning of a structural transformation whose full contours are not yet clearly defined. What is evident, however, is that the industry model that dominated for decades has entered a phase of long-term decline. This decline is not cyclical but secular in nature, rooted in the industry’s inability to keep pace with evolving consumer expectations. The assumption that past success formulas will continue to deliver future growth has become increasingly untenable.

The purpose of this analytical framework is to examine the forces reshaping the industry and to understand how both sides of the value chain—retailers and suppliers—must adapt in order to remain relevant in a fundamentally new environment. For much of the past generation, the global garment industry was characterized by relative stability. Market shares among major importing and exporting regions changed little, reinforcing a sense of predictability that encouraged incremental rather than transformative thinking.

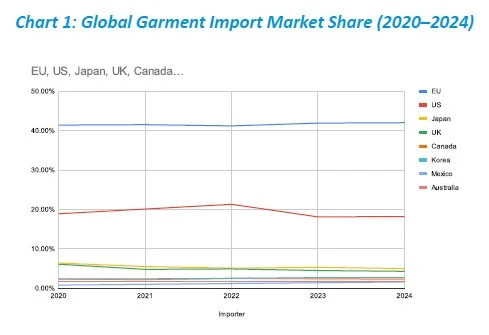

On the demand side, global garment imports have been overwhelmingly concentrated in a small number of markets. The European Union has consistently remained the dominant customer, accounting for roughly 41–42 percent of global garment imports. The United States follows at a considerable distance, with an 18–20 percent share, while all other importing markets individually remain at 5 percent or less. This concentration underscores the industry’s structural dependence on two mature consumer markets whose growth trajectories are increasingly constrained.

Chart 1: Global Garment Import Market Share (2020–2024)

| Importer | 2020 | 2021 | 2022 | 2023 | 2024 |

| EU | 41.4% | 41.5% | 41.2% | 41.9% | 42.0% |

| US | 18.9% | 20.1% | 21.3% | 18.1% | 18.2% |

| Japan | 6.4% | 5.5% | 5.1% | 5.3% | 5.0% |

| UK | 6.1% | 4.8% | 4.9% | 4.5% | 4.3% |

| Canada | 2.3% | 2.2% | 2.5% | 2.4% | 2.3% |

| Korea | 2.4% | 2.4% | 2.5% | 2.7% | 2.7% |

| Mexico | 0.8% | 1.0% | 1.2% | 1.4% | 1.6% |

| Australia | 1.7% | 1.7% | 1.7% | 1.7% | 1.7% |

| Total | 79.9% | 79.2% | 80.4% | 78.0% | 77.7% |

This data highlights not only the dominance of the EU and the US, but also the absence of meaningful diversification on the demand side. As these core markets slow, suppliers that rely almost exclusively on them face increasing vulnerability.

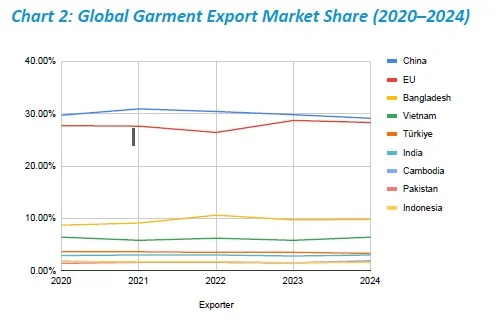

On the supply side, a similarly concentrated structure exists. China has long led global garment exports, maintaining a market share between 29 and 31 percent over the past five years. The European Union follows closely with a share ranging from 26 to 29 percent. Beyond these two, no single exporting country exceeds a 10 percent global share, although Bangladesh, Vietnam, and several other Asian producers play significant supporting roles.

Chart 2: Global Garment Export Market Share (2020–2024)

| Exporter | 2020 | 2021 | 2022 | 2023 | 2024 |

| China | 29.7% | 30.9% | 30.4% | 29.8% | 29.1% |

| EU | 27.7% | 27.6% | 26.4% | 28.7% | 28.3% |

| Bangladesh | 8.7% | 9.1% | 10.6% | 9.7% | 9.8% |

| Vietnam | 6.4% | 5.8% | 6.2% | 5.8% | 6.4% |

| Türkiye | 3.6% | 3.6% | 3.5% | 3.5% | 3.3% |

| India | 2.9% | 3.0% | 3.0% | 2.8% | 3.0% |

| Cambodia | 1.8% | 1.6% | 1.6% | 1.5% | 1.9% |

| Pakistan | 1.4% | 1.6% | 1.6% | 1.5% | 1.7% |

| Indonesia | 1.7% | 1.7% | 1.7% | 1.5% | 1.6% |

| Total | 83.8% | 84.7% | 85.1% | 84.9% | 85.1% |

While this structure once supported efficiency and scale, it is increasingly ill-suited to an environment defined by volatility and rapidly shifting consumer priorities. The stable industry of the past has effectively disappeared, replaced by a new system in which adaptability, rather than scale alone, determines success.

Also Read : Bremen Cotton Week 2026 to Shape Future of Global Cotton

Looking forward, change will unfold across multiple time horizons. In the immediate term, uncertainty itself becomes the defining characteristic. Any major structural shift introduces instability, and the more radical the change, the greater the uncertainty faced by both buyers and suppliers.

This uncertainty is amplified by short-term external forces that lie largely outside the industry’s control. The global economy is moving toward recessionary conditions, placing downward pressure on discretionary spending and reducing overall demand for garments. At the same time, shifts in US trade policy have introduced additional unpredictability, complicating long-term sourcing and investment decisions.

Over the medium term, competition within the industry will increasingly fragment along new dimensions. Product-based competition is intensifying between basic commodity garments and fast-fashion or differentiated offerings. Retail-based competition is also accelerating, as traditional brick-and-mortar channels continue to lose ground to e-commerce platforms that operate under entirely different cost and speed structures.

More disruptively, alternatives to traditional retail models are expanding, including second-hand apparel, rental services, and peer-to-peer resale platforms. These models reduce or eliminate the need for new garment production, fundamentally challenging the volume-driven logic of the traditional export industry.

In the long term, consumer choice factors will exert decisive influence over industry structure. Purchasing decisions are increasingly shaped by functionality, aesthetic value, and social status signaling rather than by price alone. Over an even longer horizon, national and cultural differences will play a growing role in determining what consumers buy, how often they buy it, and from whom.

Also Read : India–Israel FTA Talks Advance, Textile and Tech Sectors Poised to Gain

The implications for exporting countries such as Bangladesh are particularly stark. The analysis highlights a pattern of secular decline in Bangladesh’s garment exports, driven by reduced orders from its two primary customers, the EU and the US. Despite widespread recognition of the problem, responses have often been limited to vague aspirations such as introducing new products or opening new markets, without addressing the structural reasons behind declining competitiveness. Without a clear understanding of why market share is being lost in existing markets, efforts to diversify products or destinations risk repeating the same failures under new labels.

The experience of other regional competitors underscores this point. Countries such as India, Cambodia, and Pakistan are actively investing in time, capital, and external expertise to reposition their industries. In contrast, denial and inertia risk locking others into a cycle of arrested development. In a global garment industry undergoing fundamental transformation, standing still is no longer a neutral choice; it is a decision to fall behind.

In this new era, survival and success will depend not on defending the structures of the past, but on understanding the forces reshaping demand, rethinking the role of suppliers, and aligning production with the realities of a rapidly evolving consumer-driven marketplace.

With analysis and insights from David Birnbaum, Strategic Planner for the Global Garment Export Industry

{kind=link}