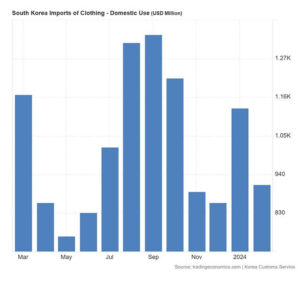

South Korea’s apparel imports fell to about $3 billion in the first quarter of 2026, with March registering a noticeably sharper decline, underscoring a sustained slowdown in one of Asia’s most closely watched consumer markets.

Data from the Korea Customs Service points to a steady contraction in inbound clothing shipments, reflecting a mix of short-term demand weakness and deeper structural changes in how South Koreans consume fashion.

The drop is unfolding in an economy that remains otherwise export-resilient, with semiconductor and industrial shipments continuing to support overall trade performance. Against this backdrop, apparel stands out as a lagging segment, increasingly disconnected from the broader export upswing.

At the retail level, caution has become more visible. Import orders have been trimmed as department stores, fashion brands, and online retailers respond to slower sales momentum. Inventory management has tightened, with businesses reluctant to overstock categories that have shown weak sell-through rates in recent seasons.

The impact is uneven across product segments. Non-knitted apparel—typically associated with more formal or fashion-driven consumption—has borne the brunt of the decline. In contrast, knitwear and basic garments have held up comparatively better, supported by the continued shift toward casualwear and comfort-oriented dressing.

This changing consumption pattern is not new, but it is becoming more entrenched. South Korean shoppers are steadily moving away from occasion-based fashion cycles toward everyday, functional clothing. That shift is gradually reshaping import composition, reducing demand for higher-margin, trend-sensitive apparel categories.

Also Read: Renewable Energy Push Stalls in Bangladesh

Industry participants also point to a growing structural undercurrent: the expansion of South Korea’s second-hand and resale clothing market. As circular fashion gains traction among younger consumers, the need for fresh imported apparel is being partially offset by increased reuse and resale activity.

Together, these shifts suggest that the current downturn is not simply cyclical. Instead, it reflects a broader recalibration of the country’s fashion ecosystem—one in which volume-driven import growth is giving way to more selective, demand-driven purchasing.

Even so, the weakness remains concentrated. Broader import flows into South Korea continue to be supported by strong demand for technology inputs, industrial goods, and energy-related products. This reinforces the view that apparel’s decline is sector-specific rather than a sign of economy-wide contraction.

Looking ahead, importers and retailers are expected to remain cautious. With consumer sentiment still subdued and pricing pressure persisting across fashion categories, procurement strategies are likely to stay conservative.

What is emerging, therefore, is not just a temporary dip in shipments, but a more gradual restructuring of South Korea’s apparel import landscape—one defined less by expansion, and more by adjustment to a changing consumer base and retail reality.

{kind=link}