Sri Lanka’s apparel exports started 2026 on a softer footing, with total shipments falling nearly 3% in January amid subdued demand from key markets, data from the Joint Apparel Association Forum (JAAF) showed. The performance highlights ongoing headwinds for one of the country’s most export-dependent industries, even as preferential trade access supports resilience in select destinations.

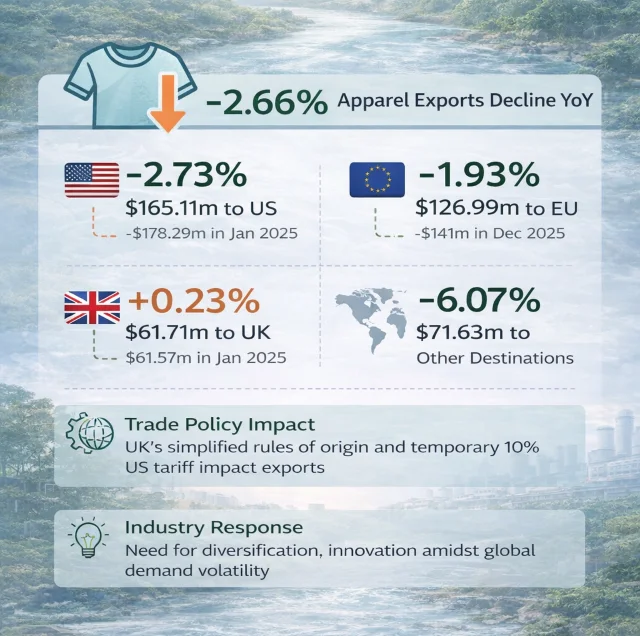

According to JAAF figures, Sri Lanka’s apparel exports declined 2.66% year-on-year in January 2026, totaling $425.44 million compared with $437.07 million in the same month last year. The decline reflects continued volatility in global orders and a cautious footing among major buyers, particularly in the United States and the European Union.

Export shipments to the United States, Sri Lanka’s largest apparel market, fell 2.73% to $165.11 million in January 2026 from $178.29 million a year earlier. Similarly, exports to the EU (excluding the UK) slid 1.93% to $126.99 million. Other destinations, including markets in Asia and Latin America, also recorded weaker performance, with shipments down 6.07% to $71.63 million.

Despite these declines, Sri Lanka’s apparel exports to the United Kingdom posted a modest gain. Shipments to the UK rose 0.23% to $61.71 million in January 2026, following a sharper 12.95% rise to $55.12 million in December 2025. Industry leaders and trade analysts attribute this relative stability to recent trade policy changes that are making Sri Lankan products more competitive in the British market.

Trade Policies and Market Dynamics

The contrasting performance across regions underscores how trade policy shifts and buyer behaviour are shaping Sri Lanka’s apparel exports. On Jan. 1, 2026, the UK’s revised Developing Countries Trading Scheme (DCTS) came into effect, easing rules of origin requirements. Under the new system, Sri Lankan manufacturers can export clothing tariff-free into the UK even if they source raw materials globally, removing previous restrictions that limited fabric sourcing to designated Asian countries.

This enhanced flexibility is significant for Sri Lanka’s apparel sector, which relies on a globally integrated supply chain for fabrics, trims and other inputs. The ability to qualify for duty-free access without restrictive sourcing conditions strengthens the country’s competitive position, especially for fast-fashion programmes and smaller production runs where flexibility in input sourcing is critical.

Trade experts say the UK’s preferential access could help Sri Lankan exporters build momentum in a market that accounts for a sizeable share of shipments and where demand has shown relative resilience compared with the US and EU.

In contrast, US demand has faced mixed signals. In the short term, the introduction of a uniform temporary 10% tariff on select imports was intended to bring clarity compared with prior country-specific duty rates. However, retailers and brands in the US have been slow to ramp up orders, reflecting broader inventory management strategies and caution ahead of spring and summer retail seasons. The slower pace of orders from US buyers tends to impact mid-range apparel suppliers like Sri Lanka more acutely than high-end or highly differentiated producers.

Also read: Sri Lanka’s Apparel Industry Gains Momentum as Exports Climb 5.4%

Structural Challenges and Industry Response

The January export figures reinforce structural challenges facing Sri Lanka’s apparel industry. Global apparel demand remains uneven as consumers in key markets balance inflationary pressures, shifting fashion trends and supply chain recalibration. These dynamics have compelled buyers to tighten order books and delay commitments, putting pressure on export volumes and factory utilisation rates.

JAAF has highlighted the need for Sri Lanka to enhance diversification and competitiveness, pointing to strategies that include expanding into new markets, upgrading product offerings and improving operational efficiency. For an industry that contributes significantly to national foreign exchange earnings and employment, sustaining competitiveness in a fragmented global apparel landscape is critical.

Market diversification is increasingly seen as a strategic imperative. Growth opportunities in emerging markets, such as the Middle East, parts of Africa and select Asian countries, could offer alternative demand drivers as traditional Western markets fluctuate. However, penetration into these markets requires tailored product mixes, competitive pricing and stronger logistical support.

Looking ahead, Sri Lanka’s apparel exporters are taking a cautiously optimistic view. The goal for many firms is not just to stabilise volumes but to climb the value chain into higher-margin segments such as performance wear, sustainable and ethically produced garments, and specialised fashion categories.

The relative stability in the UK market, supported by trade policy reform, offers a tangible example of how external policy levers can influence export performance. If Sri Lanka can leverage preferential access and strengthen relationships with UK buyers, it may help offset slower demand in the US and EU.

Nevertheless, the January data serves as an early indicator of ongoing challenges. With uneven global demand and competitive pressures from other supply hubs, Sri Lanka’s apparel sector will need to balance market diversification, productivity gains and product innovation to maintain its footprint in global sourcing networks.

The industry’s focus on resilience, coupled with strategic trade advantages, may position it for modest recovery in the coming months, provided global consumption patterns stabilise and buyers signal stronger commitments ahead of peak sourcing seasons later in 2026.

{kind=link}